Corporate Tax Rates: Analysis of the TCJA’s Impact

Corporate tax rates have become a focal point of debate in the U.S. economic landscape, especially in light of findings from recent studies on the Tax Cuts and Jobs Act (TCJA) of 2017. As this legislative measure nears expiration, the discussions around potential reforms are intensifying, with GOP and Democratic leaders vying for public support. The economic impact of tax cuts under the TCJA has been scrutinized, revealing modest increases in wages and business investment growth, while also highlighting significant decreases in corporate tax revenues. Tax policy analysis shows that while proponents of the law argue for further cuts, evidence suggests that maintaining higher corporate tax rates could yield better long-term benefits for the economy. Ultimately, this ongoing dialogue plays a crucial role in shaping the future of corporate tax reform and its implications for American businesses and taxpayers alike.

The discussion surrounding corporate taxation is a contentious issue that encapsulates various economic theories and political stances. Recently, lawmakers have rekindled interest in business tax regulation as critical components of broader financial strategies, particularly in the context of the upcoming expiration of the TCJA provisions. This complex web of tax policy encapsulates the tension between advocating for lower corporate taxes to stimulate growth and the necessity of increased rates to bolster government revenue. The ramifications of such reforms are significant, as they not only affect business investment but also ripple through the labor market and impact wage growth. As elections loom, understanding the intricacies of this tax debate could guide voters’ choices and influence the next steps in fiscal planning.

The Economic Impact of the Tax Cuts and Jobs Act

The Tax Cuts and Jobs Act (TCJA) of 2017 had significant implications for the U.S. economy, particularly regarding investment and corporate behavior. One of the main goals of the TCJA was to enhance business investment growth by reducing the corporate tax rate from 35% to 21%. This drastic cut aimed to provide businesses with more capital to invest in infrastructure, technology, and human resources. Studies indicate that this reduction did lead to a modest uptick in capital investments by approximately 11%. However, the study by Chodorow-Reich and his colleagues shows that the expected massive revenue growth to offset these cuts did not materialize, implicating the complexities of tax policy analysis in real-world economic scenarios.

Moreover, while proponents of the TCJA argued that such cuts were necessary to keep American corporations competitive in a globalized economy, the actual results present a more nuanced picture. The law’s provisions intended to stimulate investment did lead companies to modify their spending behaviors, but the overall economic impact was less pronounced than anticipated. The anticipated substantial wage increases did occur, but only modestly, with data showing an average increase of approximately $750 per employee—far lower than the initial projections of up to $9,000. Such outcomes spark important discussions on the efficacy of broad corporate tax reform in achieving the desired economic revitalization.

Debating Corporate Tax Rates: A Partisan Battlefield

As the expiration of key provisions in the Tax Cuts and Jobs Act approaches, corporate tax rates are once more at the center of a heated partisan debate. On one side, Democrats advocate for an increase in corporate tax rates as a means to fund essential social programs, while Republicans maintain that further reductions will promote economic growth and investment. This political tug-of-war has significant implications for both corporate tax policy and broader fiscal health. The divergence in beliefs reflects a larger ideological split regarding whether higher taxes stifle economic progress or if equitable contributions from corporations bolster public welfare.

The battle over corporate tax rates is not merely a political game; it is tied to the broader economic consequences of fiscal policy. Studies contend that raising corporate taxes could prove detrimental to business investments and stifle innovation, which is crucial for job creation and economic expansion. Conversely, proponents of increasing corporate taxes argue that it is essential for ensuring that corporations contribute their fair share to the economy, particularly when they have benefited from reduced rates in recent years. This contentious environment underscores the need for comprehensive tax policy analysis that considers both short-term economic effects and long-term fiscal sustainability.

Chodorow-Reich’s research indicates that there are more effective ways to foster growth than simply altering corporate tax rates. His findings suggest that targeted provisions, such as immediate expensing of new investments, could yield better outcomes for business growth and job creation. As legislators grapple with these critical issues leading up to 2025, the discourse surrounding corporate tax rates will inevitably shape the future of U.S. tax policy and its alignment with economic goals.

Understanding Business Investment Growth Post-TCJA

The profound change in business investment growth following the TCJA is an essential aspect of understanding the law’s outcomes. The immediate reduction of corporate tax rates was aimed at incentivizing businesses to reinvest savings directly into their operations and workforce. This strategic shift was grounded in the notion that lower tax obligations would allow companies to allocate more resources towards capital expenditures and innovation. However, the key question arises: did the TCJA achieve its objective? Evidence collected by Chodorow-Reich and his team suggests that while investment growth did occur, it was not as sweeping as anticipated.

Interestingly, their comprehensive analysis points to expired tax provisions concerning investment expensing that had a more favorable impact on driving investments than the rate cuts themselves. This observation raises critical considerations for future tax policies, especially as lawmakers seek to strike a balance between competitive corporate tax rates and providing necessary revenue for public services. As businesses re-evaluate their investment strategies in light of potential increases in corporate tax rates, understanding the dynamics of pre-and post-TCJA investment behavior can guide effective tax reforms that genuinely stimulate economic growth.

The Role of Fiscal Responsibility in Tax Reform

One of the most critical discussions emerging from the TCJA’s evaluation is the degree of fiscal responsibility that government must uphold when enacting tax reforms. Tax policy is inherently tied to national revenue, and the deep cuts introduced by the TCJA raised alarms over future deficits. The projected loss of $100 to $150 billion in annual federal corporate tax revenue posed questions about how these gaps would be filled without exacerbating the budget woes faced by the government. The urgency behind balancing tax cuts with fiscal sustainability must guide future discussions on tax law reforms.

Assessing the implications of the TCJA reveals that while corporate tax cuts were presented as a pathway to spur economic growth, the long-term fiscal health of the nation may hinge on finding a compromise that supports business investment without undermining public resources. An essential part of this conversation will involve exploring innovative policy proposals that not only raise corporate tax rates, but also restore more effective provisions aimed at encouraging investment and growth while ensuring that essential public services can be funded. The intersection of fiscal responsibility and economic vitality remains at the forefront of ongoing tax policy debates.

Targeting Investment through Tax Policy Design

As the discussions surrounding corporate tax rates evolve, a critical component will be the design of tax policies that effectively target business investment. Research conducted by Chodorow-Reich et al. indicates that while statuary corporate tax reductions can stimulate investment, measures such as targeted expensing provisions yield even more substantial returns. These insights reveal the importance of tailoring fiscal policy to address the specific needs of an economy driven by innovation and investment. Basing tax policy reforms on empirical evidence can guide lawmakers in constructing a more efficient tax landscape that fosters sustainable growth.

Moreover, as lawmakers prepare for potential reforms in the 2025 budget cycle, consideration must be given to integrating provisions that directly incentivize productive capital investment. By adopting a comprehensive approach that considers various mechanisms aimed at rewarding businesses for expanding their operations, tax reforms can be designed to not only enhance immediate growth but also to lay the groundwork for long-term economic flourishing. This nuanced approach can effectively align tax incentives with the emerging needs of the modern economy, ensuring that reforms uphold both fiscal soundness and investment stimulation.

Long-term Projections of Corporate Tax Revenue

The long-term projections of corporate tax revenue stemming from President Trump’s TCJA illustrate the complexity of forecasting fiscal outcomes amid changing economic climates. Initially, the forecasts suggested that the drastic cuts to corporate tax rates would precipitate a significant revenue decline. However, as the economy underwent transformations during the COVID-19 pandemic, corporate profits soared unexpectedly, leading to a surprising rebound in tax revenues. Understanding the trajectories of these revenues will be crucial for future reforms, particularly as legislators consider options to enhance fiscal stability by potentially raising corporate tax rates.

The unexpected growth in corporate tax revenues in the wake of the TCJA challenges earlier assumptions regarding the direct correlations between tax rates and revenue generation. Research indicates that external factors, such as shifts in global corporate behavior and changing economic conditions, play crucial roles in shaping revenue outcomes. As the political landscape shifts and tax policy debates intensify, it’s vital to maintain a statistically sound approach in tax policy analysis, ensuring predictive models adequately reflect the realities of the business environment. Through careful scrutiny of historical data and trends, decision-makers can craft tax policies that adapt to economic fluctuations while securing necessary revenue streams.

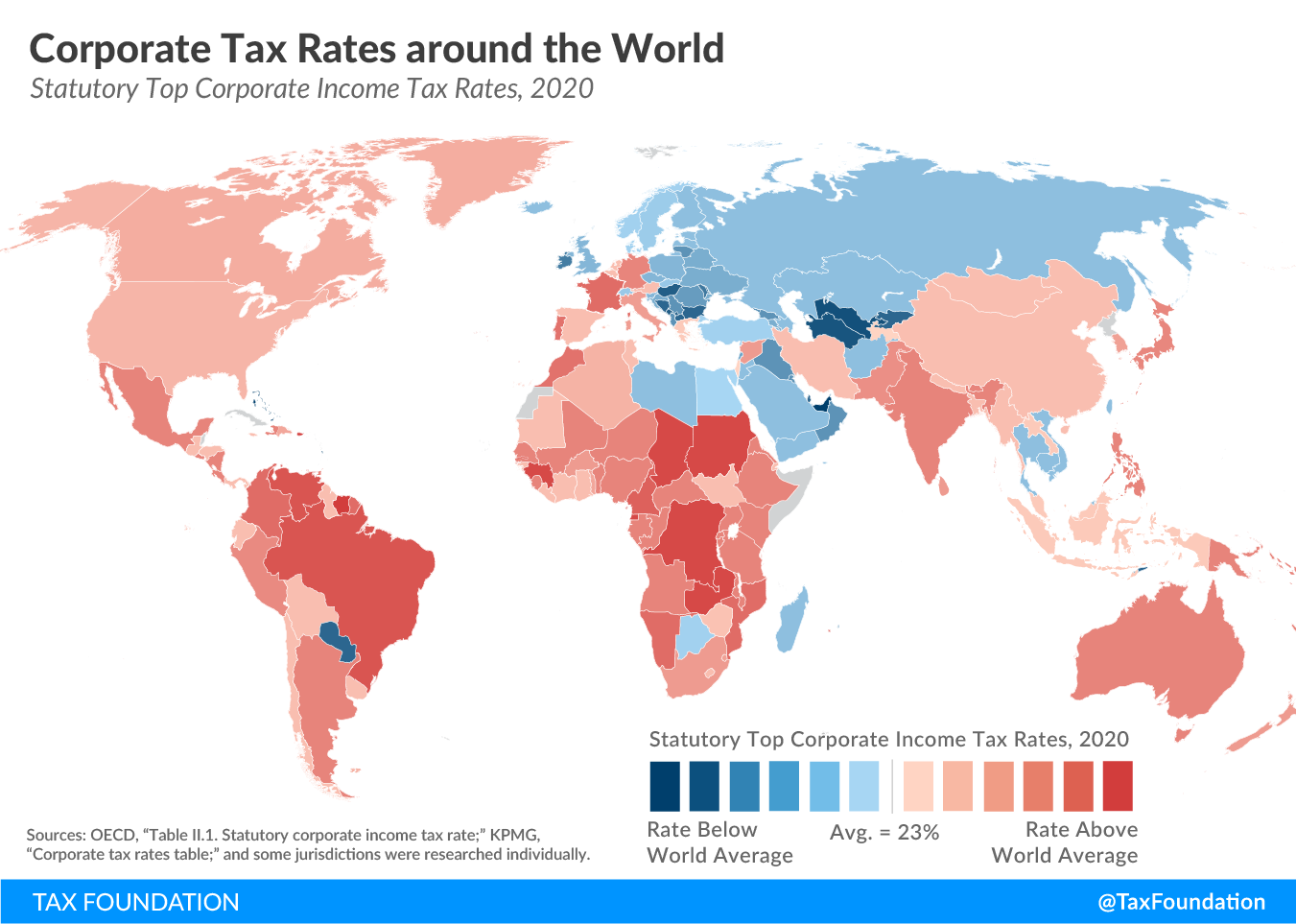

Corporate Tax Policy and International Competitiveness

In an era of increasing globalization, corporate tax policy directly influences national competitiveness. The TCJA positioned the U.S. more favorably against international peers by reducing the corporate tax rate. Such competitiveness is essential as businesses operate on a global stage, navigating various regimes that impact their financial decisions. The necessity for a competitive corporate tax structure cannot be overstated, especially as other countries adjust their rates in response to economic pressures. Moving forward, it is paramount for lawmakers to continually assess the effectiveness of the U.S. corporate tax framework in fostering international competitiveness while also addressing domestic fiscal requirements.

However, the ongoing debate surrounding corporate tax rates highlights a delicate balancing act. While nations attempt to lower tax burdens to attract investment, there is a concurrent need for adequate funding of public services that support economic activities. The implications of changing corporate rates can ripple through global markets, influencing where corporations choose to invest and establish operations. Thus, future tax policies must not only prioritize competitiveness but also engage with broader economic virtues—ensuring that the need for investment aligns with the responsibility of maintaining a healthy and robust national economy.

Reflections on Bipartisan Tax Policy Initiatives

A critical reflection on the TCJA and subsequent tax policy proposals reveals the challenges of achieving bipartisan support in tax reforms. With both parties holding fundamentally different viewpoints on corporate taxation, finding solutions that address diverse interests becomes increasingly complex. The research by Chodorow-Reich and colleagues emphasizes the value of collaborative approaches that transcend partisan lines. Crafting thoughtful tax reforms requires acknowledging the intricacies of economic outcomes while engaging in cooperative dialogue across the political spectrum.

As lawmakers confront the urgent need for tax reform in light of expiring provisions, the lessons learned from the TCJA may inform new initiatives. Prioritizing the development of tax policies that emphasize growth, sustainability, and equity can serve as a foundation for uniting disparate political interests. The overarching goal should be to foster an environment conducive to both business investment and social equity, ultimately leading to a more prosperous economy. By reframing tax policy discussions through the lens of federal responsibility and effective investment planning, it may be possible to create a framework that resonates across party lines.

Frequently Asked Questions

What are the implications of corporate tax rates following the Tax Cuts and Jobs Act?

The Tax Cuts and Jobs Act (TCJA) of 2017 significantly lowered the U.S. corporate tax rate from 35% to 21%. This reform aimed to stimulate business investment growth and increase wages for employees. However, while there was a modest increase in capital investment and wages, analysis suggests the resultant tax revenue drop was substantial, challenging the belief that tax cuts alone can boost corporate growth significantly.

How did the corporate tax rates under the TCJA affect business investment growth?

Under the TCJA, corporate tax rates were reduced, which reportedly led to an 11% increase in capital investments. The legislation included provisions for immediate expensing of new capital investments, which proved more effective in encouraging growth than the mere reduction in statutory rates. This indicates that targeted tax policy can have a more pronounced impact on business investment.

Is there evidence that corporate tax reform led to wage increases?

While proponents of the TCJA anticipated substantial wage increases—between $4,000 and $9,000 per full-time employee—the empirical data collected suggests the increase was closer to $750 annually. This disparity highlights the complexities of predicting direct economic outcomes from corporate tax policy changes.

What challenges does Congress face regarding corporate tax rates as provisions from the TCJA expire?

As provisions from the TCJA are set to sunset, Congress will need to address the potential budget shortfall caused by reduced corporate tax revenue. The ongoing debate about whether to raise corporate tax rates or extend certain favorable expensing provisions creates a complex tax policy environment that stakeholders must navigate carefully.

How has the economic impact of tax cuts influenced corporate tax policy discussions?

The economic impact of the TCJA continues to shape discussions about corporate tax policy. Stakeholders analyze the balance between lowering corporate rates to spur investment versus raising them to ensure adequate tax revenue. Research indicates that while tax cuts alone do not necessarily drive business growth, targeted reforms can lead to improved investment and wage outcomes.

What lessons can policymakers learn from the corporate tax rates established by the TCJA?

Policymakers can learn that corporate tax rates, when reformed effectively, can influence business behavior, particularly in terms of investment and hiring. Evidence suggests that measures such as targeted expensing could yield better returns on investment growth than broad rate cuts, guiding future corporate tax reform discussions.

What are the long-term effects of the TCJA on corporate tax revenue?

Initially, the TCJA resulted in a dramatic reduction in corporate tax revenue by approximately 40%. However, starting in 2020, revenue from corporate taxes began to recover, driven by soaring business profits. This rebound underscores the importance of understanding external economic factors, such as changes in global corporate tax strategies, when evaluating the effectiveness of corporate tax policy.

What role does tax policy analysis play in shaping future corporate tax rates?

Tax policy analysis is crucial in assessing the effectiveness of existing corporate tax rates and proposing future reforms. By analyzing data on investment behavior, wage impacts, and tax revenue, economists and policymakers can develop more nuanced and effective corporate tax strategies that stimulate economic growth while ensuring a sustainable revenue base.

| Key Points |

|---|

| Congress is gearing up for a tax battle in 2025 regarding corporate taxes and household provisions from the 2017 Tax Cuts and Jobs Act (TCJA). |

| The TCJA significantly lowered the corporate tax rate from 35% to 21%, aimed at stimulating business investment and growth. |

| Research indicates that corporate tax cuts did not generate the expected increase in wage growth, with estimates revised down to around $750 annually instead of projected higher figures. |

| Corporate tax revenue initially dropped 40% following the TCJA but later rebounded due to unexpected rises in corporate profits during the pandemic. |

| The debate is ongoing between raising corporate tax rates versus extending provisions encouraging capital investment; both sides claim to support economic growth. |

| Gabriel Chodorow-Reich’s study provides insight into the effectiveness of tax policy on corporate behavior and raises important questions about future tax reforms. |

Summary

Corporate Tax Rates are at the heart of a contentious debate as Congress heads towards 2025. With the expiration of key provisions from the 2017 Tax Cuts and Jobs Act approaching, both parties are vying for their approach to taxation. While some advocate for higher corporate tax rates to support social programs, others believe that further cuts will alleviate financial pressures on businesses and encourage growth. The data reveals that while the TCJA boosted business investments, it also led to a notable decline in tax revenue, prompting discussions on more effective reform that balances revenue generation with economic growth.